By Vincent Howard, CPA | Managing Partner, Howard, Howard and Hodges | Skillability for Accounting Firms

Last updated: 2026 | 16-minute read

The Short Answer (TL;DR)

Accounting is not a dying profession. It is a splitting one. Three forces are colliding at once — a collapsing talent pipeline (300,000+ accountants left the profession between 2019 and 2021, with a projected 120,000-professional gap by 2027), AI automation absorbing the data-entry layer of the work within three to five years, and surging small-business demand for advisory guidance that software cannot provide. The result is a profession dividing into two: a shrinking, commoditized compliance-processing layer with declining margins and a vanishing workforce — and an expanding, high-margin advisory layer that pays more, retains better, and cannot be automated. The dividing line between firms that end up on the right side and firms that don’t is not size, location, or even technology. It is development infrastructure: whether a firm can systematically convert the people it has into the professionals the next decade requires. Firms that build that capability between now and roughly 2028 will own the transition. Firms that wait will arrive at the future with a workforce trained for jobs that no longer exist.

That’s the thesis. Here is the evidence, the anatomy of the firm that wins, and the uncomfortable math of the window you’re standing in.

Who I Am and Why You Should Listen

I’ve been in public accounting since 1990. I founded my own firm in 1993, merged it in 2001 to form Howard, Howard and Hodges, and grew it from three people to 50 staff across four locations and multiple states.

I should also tell you something about how I’m wired, because it’s relevant to whether you should trust a prediction from me. On the DISC personality assessment, where most accounting managers score in the high 80s or 90s on stability — the trait that resists change — I scored a three. I have spent my entire career constitutionally incapable of accepting “that’s how we’ve always done it.” That disposition built a 50-person firm. It also built, as a side effect of one impulsive phone call about renting a racetrack, what became the largest track-day organization in the United States. I don’t say that to impress you. I say it because the analysis you’re about to read comes from someone whose bias runs toward seeing disruption early — sometimes too early — and who has learned, over 35 years, to check that bias against data.

The data I get to check it against is unusual. Since 2020, I’ve built and operated a training platform that more than a thousand accounting professionals across dozens of PASBA member firms have moved through. I can see — in completion times, assessment scores, and progression patterns — exactly what the profession’s incoming workforce can and cannot do, and exactly how fast they can be developed into something more. Most people writing about the future of accounting are extrapolating from headlines. I’m extrapolating from a thousand measured careers.

And one more credential, the kind that doesn’t fit on a bio: I have already lived through one version of this profession ending. In 2001, the 80-hour-tax-season model of public accounting broke my family’s patience, and we responded by firing half our client list and rebuilding the firm around a different economic model entirely. Everyone said it was reckless. Within 18 months we were larger than before. I have personally bet a firm on the proposition that the standard model was dying — and won. I’m about to tell you why I’d make the same bet again, bigger, today.

Three Collisions, One Outcome

Professions don’t transform because of one trend. They transform when multiple trends arrive at the same intersection at the same time. Accounting has three inbound, and they are closer than most managing partners want to believe.

Collision One: The pipeline didn’t shrink. It broke.

The numbers deserve to be stated plainly, because the profession has developed a habit of euphemizing them. More than 300,000 accountants and auditors left the profession between 2019 and 2021 — and the graduates coming up behind them aren’t replacing them. Projections put the talent gap at 120,000 professionals by 2027, with nearly 40% of CPAs approaching retirement age. Meanwhile the staff who do exist keep moving: public accounting loses 41% of its people within three years of hire.

The profession’s institutional response — rethinking the 150-hour rule, alternative licensure pathways, recruiting campaigns aimed at students — is real and probably necessary. It is also slow. Pipeline reforms enacted now produce licensed professionals in five to seven years. Your capacity problem is this tax season.

Here’s what the pipeline collapse actually means at the firm level, stated as bluntly as I can: the strategy of buying experienced talent is ending. Not getting harder. Ending. When 120,000 professionals simply don’t exist, the recruiter with the $20,000 placement fee isn’t expensive — he’s selling inventory that isn’t there. The only reliable source of capable accounting professionals over the next decade will be the ones firms manufacture themselves, from higher-aptitude raw material, through systematic development. Firms with that manufacturing capability will have talent. Firms without it will have job postings.

Collision Two: AI is eating the bottom of the profession — and only the bottom

I’ve been saying this in webinars and at conferences for several years now, and I’ll put it in writing without hedging: data-entry bookkeeping, as an occupation, has three to five years left. Probably less. Automated bank feeds, machine-learning categorization, auto-reconciliation — the key-punching layer of our work is already mostly gone in well-run firms, and the remainder is disappearing on a schedule no one in this profession controls.

Most commentary stops there and writes the obituary for the whole profession. That’s where the commentary is wrong, and where actually doing this work for 35 years matters.

What AI absorbs is the backward-looking, rules-following layer: recording what happened, categorizing it, reconciling it. What AI cannot absorb — not in any deployable, fiduciary-grade form — is the forward-looking, judgment-bearing layer: noticing that a client’s margin compression means their pricing model is broken, recognizing that a partnership transfer without a Section 754 election is leaving money on the table, sitting across from a business owner in October and walking them through five year-end scenarios while reading which one they actually have the stomach for. Software flags. Humans advise. The advisory layer isn’t shrinking under AI — it’s expanding, because every hour automation strips out of data processing is an hour of accountant capacity that can be redeployed up the value chain, and because small business owners drowning in software dashboards need more interpretation, not less.

So the real AI story in accounting is not replacement. It is relocation. The work is moving up. The only question — the entire question — is whether your people can move up with it.

Collision Three: The clients already voted

While the profession debates its future, the market quietly decided. Compliance work — the return, the monthly financials, the payroll filings — has been commoditized by the same software wave, and clients price it accordingly. Advisory work commands a different economy entirely: the compliance client paying $3,000 to $5,000 a year becomes, on a proactive advisory retainer, a $12,000 to $18,000 relationship. Same client. Same data. The difference is purely whether someone at the firm has the capability to surface the value sitting in files the firm already touches every month.

Read those three collisions together and the conclusion assembles itself: the profession’s low-value work is being automated, its workforce supply is broken, and its high-value work is in surplus demand. That is not a dying profession. That is a profession in the middle of the most asymmetric opportunity transfer I have seen in 35 years — from firms that process to firms that develop.

The Split: Two Professions Wearing One Name

By roughly 2031, “accounting firm” will describe two fundamentally different businesses that happen to share a license.

The Processing Firm will still exist — running compliance volume on thin margins, competing on price against software and offshore capacity, staffed by a shrinking pool of people doing work with a known expiration date, owned by partners who are personally the ceiling on everything because no layer beneath them was ever developed. These firms won’t dramatically collapse. They’ll do something quieter: stagnate, lose their best people to the other kind of firm, and eventually sell — at processing-firm multiples — to consolidators.

The Development Firm is the other species, and I described its anatomy in detail because I’ve been deliberately building toward it for years. It looks like this:

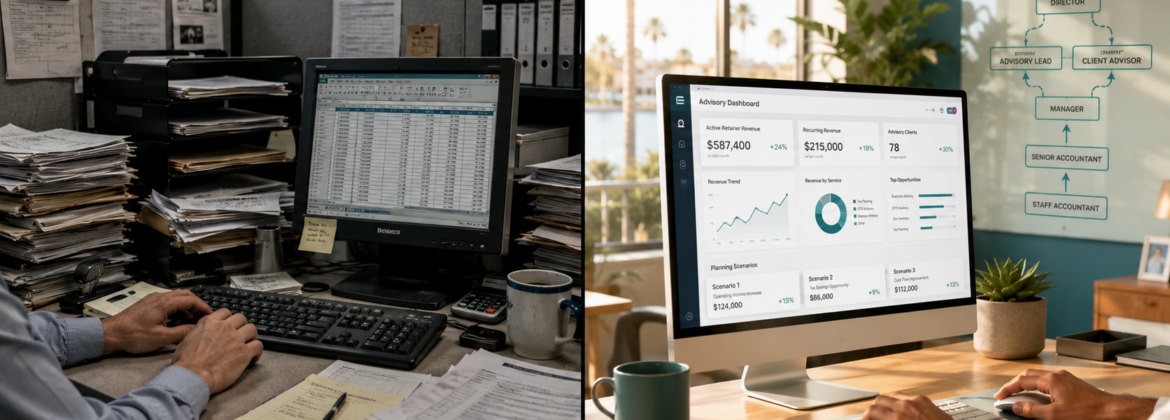

Its staffing pyramid is inverted from today’s. Where a 25-person firm in 2026 runs eight to ten bookkeepers feeding a compliance engine, the 2031 development firm runs four or five — each managing and validating AI-processed output rather than producing entries — and six to eight people operating as what I call accounting consultants: professionals who read financials for story rather than just accuracy, spot planning opportunities, and carry client conversations that today escalate to a partner.

Its managers stopped being answer desks. With the mechanical layer handled by structured training infrastructure and AI handling first-pass processing, the manager’s week shifted from error-correction and basic-question triage to the only work that justifies a manager: quality elevation, judgment coaching, and developing the next layer of advisors. Review changed from “catch the mistakes” to “find the missed opportunity.”

Its hiring became a manufacturing process. Pre-employment testing verifies aptitude before any offer. Structured onboarding produces independent productivity in under 30 days, with objective milestone data replacing 90 days of gut feel. Mis-hires surface in week one — at one of our member firms, a mismatched hire whose module times ran four times the firm benchmark resigned on day six, before either side had sunk a quarter into the mistake. The development firm doesn’t make better hiring bets. It made hiring stop being a bet.

Its people stay. Because the single biggest controllable driver of turnover — the invisible future — got solved structurally. Research already shows firms with structured development reduce first-year turnover by 30 to 40 percent, and CPA-track staff retain at 73% versus 49% for peers without a credential pathway. The development firm’s bookkeeper from 2026 is its advisor in 2031, earning advisor compensation, and every junior person in the building can see that path because it’s written down with milestones on it. Recruiters can’t sell what the firm already provides.

Its economics changed shape. Revenue per professional climbs not because rates went up but because the work mix moved up — a larger share of hours billing at advisory value instead of processing value, on retainers instead of engagements. The partner’s calendar, the original bottleneck of the entire profession, finally decongested: not because the partner works more, but because three layers of capability now exist beneath them.

Here’s the part I need you to sit with: every single component of that firm is buildable today, with infrastructure that already exists. Nothing in that description requires a technology that hasn’t shipped or a regulation that hasn’t passed. The 2031 development firm is simply a 2026 firm that made one structural decision and then compounded it for five years.

Which is exactly why the window matters.

The Window: Why 2026–2028 Decides This

Transformations like this one have a cruel property: the decision period is much shorter than the transition period. The split will take until 2031 to become obvious. The choice of which side you’re on is being made now, for three compounding reasons.

First, development has a lead time. Converting a compliance processor into a genuine advisor — financial statement analysis, advanced tax scenarios, proactive client communication — is a structured 12-to-24-month journey even with the best infrastructure. A firm that starts in 2026 has advisory capacity producing revenue by 2028 and a deep bench by 2031. A firm that starts in 2029 spends the critical years training while its competitors are already monetizing — and is recruiting its raw material from a labor pool that’s three years thinner.

Second, the talent math punishes the late. The shrinking pipeline means the firms that can develop people will increasingly be the only firms that have people. And retention compounds the gap: every year a development firm holds its 30-to-40-percent turnover advantage, the processing firms across town are re-staffing, re-training (badly, via shadowing), and re-losing the same seats — burning roughly $9,500 per hire on onboarding drag and a quarter-million annually on replacement costs while the development firm’s institutional knowledge deepens uninterrupted.

Third, your best people can see the split too. Your sharpest bookkeeper reads the same AI headlines you do. Right now, today, she is deciding whether her future exists at your firm. If you have a funded, visible pathway that takes her from data processing to advisory work, you’ve answered the question and kept her. If your answer is “don’t worry” — she’ll find a firm whose answer is a curriculum. The first asset the processing firms will lose isn’t clients. It’s exactly the people they’d have needed to become something else.

I watched a version of this window once before. In 2001, when we rebuilt our firm around sustainable hours and better clients, the conventional wisdom said you couldn’t run a profitable practice that way. The firms that moved early on that model spent two decades recruiting against firms that couldn’t match it. The firms that waited until the model was proven found that the advantage had already been banked by someone else. Windows don’t announce themselves. They just close.

What This Looks Like on Monday Morning

Grand theses are cheap. Here is the actual sequence, compressed from everything I’ve built and watched work:

1. Run the two audits — one hour, brutal honesty required. First: what percentage of your firm’s current labor hours are backward-looking processing that automation will absorb? At most firms it’s 40 to 60 percent. Second: how much advisory revenue is latent in your existing client files — the planning opportunities your current staff sees but isn’t trained to surface, or doesn’t see at all? Those two numbers are your exposure and your upside. Most partners have never written either one down.

2. Install the manufacturing line before you need it. Structured, gated, real-software onboarding that takes a new hire to independent productivity in under 30 days, with pre-employment testing in front of every offer. This is the foundation everything else stands on — it’s what frees senior capacity, what makes hiring scalable in a broken labor market, and what generates the objective data the rest of the system runs on.

3. Pick your first two converts. Not your whole staff — your two highest-aptitude compliance people who show appetite for client-facing work. Put them on the advisory development track: financial statement analysis, the advanced tax scenarios that drive planning conversations (S-corp compensation, entity optimization, the Section 754s and 1202s that processors never surface), and a structured monthly client-contact discipline. Your platform data will tell you within months whether you picked right.

4. Convert two clients each, then compound. Two existing compliance clients per developing advisor, moved to proactive advisory retainers in year one. At the $9,000-to-$13,000 per-client uplift the math reliably produces, four conversions fund the entire infrastructure several times over — and you haven’t acquired a single new client. Everything after that is the compounding phase: more converts, more conversions, a visibly different firm by year three.

5. Tell your people the plan — explicitly. The retention value of this transformation is only collected if your staff knows it’s happening. Show them the pathway with their name on it. The announcement that “this firm is building its people into the next version of this profession” is worth more than any raise you were considering, and it costs a staff meeting.

Frequently Asked Questions

Is accounting a dying profession?

No — but half of it is. The data-entry and routine compliance layer of accounting is being absorbed by automation on a three-to-five-year horizon, and the workforce supplying it is shrinking (300,000+ professionals left between 2019 and 2021, with a projected 120,000-person gap by 2027). Simultaneously, the advisory layer — forward-looking tax planning, financial analysis, business guidance — is expanding, commands premium retainer pricing, and cannot be automated at fiduciary grade. The profession is splitting rather than dying: firms and professionals who move up the value chain face the strongest market in decades, while those anchored to processing work face commoditization. The dividing factor is development infrastructure, not firm size or geography.

Will AI replace bookkeepers?

AI will replace data-entry bookkeeping — the recording, categorizing, and reconciling layer — and substantially already has in well-run firms. It will not replace the judgment layer: interpreting financial statements, spotting anomalies and planning opportunities, advising clients, and managing the exceptions automation flags. The realistic forecast is relocation rather than elimination: bookkeepers who upskill into analysis and advisory roles become more valuable as automation frees their capacity, while bookkeepers whose only skill is data processing face displacement within three to five years. The determining variable is whether their firm provides a structured upskilling pathway before the transition completes.

What accounting jobs are safe from AI?

The safe layer is wherever judgment, relationships, and forward-looking analysis live: tax planning and scenario modeling, financial statement interpretation and advisory, complex transactions (entity restructuring, partnership basis issues, M&A support), client relationship management, and review/quality roles that evaluate AI-assisted output. The exposed layer is backward-looking and rules-based: transaction entry, categorization, routine reconciliation, and basic return assembly. The practical career strategy — for individuals and for firms staffing them — is deliberate movement from the exposed layer to the safe layer while automation handles the transition’s mechanical side.

Why are fewer people becoming CPAs?

Several compounding causes: the 150-hour education requirement added a fifth year of schooling cost ahead of a starting salary that lags other business careers; the profession’s reputation for brutal busy-season hours deters graduates who watched prior generations burn out; retirements are removing experienced CPAs faster than entrants replace them (roughly 40% of CPAs are at or near retirement age); and 300,000+ professionals left accounting between 2019 and 2021. The institutional response — alternative licensure pathways and reconsideration of the 150-hour rule in many states — is underway but slow-acting, which means firms cannot wait for the pipeline to refill and must develop talent internally to staff the next decade.

How do accounting firms prepare for AI?

Four moves, in sequence: (1) audit your exposure — quantify what share of current labor hours is automatable processing versus judgment work; (2) install structured training infrastructure so new hires reach productivity in under 30 days and hiring stops depending on a broken experienced-talent market; (3) systematically upskill existing compliance staff into advisory capability — financial analysis, planning scenarios, proactive client communication — before automation makes their current roles obsolete; (4) convert existing compliance clients to advisory retainers as that capability comes online, which typically lifts per-client revenue from the $3,000–$5,000 range to $12,000–$18,000 and funds the entire transition from clients the firm already serves. Firms that complete this between 2026 and 2028 own the transition; firms that wait will be training while competitors are monetizing.

What is the future of small accounting firms?

Stronger than the headlines suggest — for the ones that adapt. Small firms hold structural advantages in the split: closer client relationships (the raw material of advisory revenue), faster decision cycles than large firms, and notably better retention (firms under $5 million in revenue ran 8.1% turnover in 2025 versus 14.6% at $75M+ firms). The threat to small firms isn’t size; it’s the owner-as-bottleneck model, where all judgment work concentrates in one or two partners. Small firms that build development infrastructure — converting their compliance staff into an advisory layer beneath the partners — become the most defensible businesses in the profession. Those that remain processing shops face commoditized pricing and eventual consolidation.

The Bottom Line

Every managing partner reading this already feels the three collisions — the hires you can’t find, the software release notes that keep absorbing another slice of the work, the clients asking questions that deserve better answers than a return. The mistake is reading them as three separate problems. They are one event: the profession splitting into a side that processes and a side that advises, with a one-time, asymmetric transfer of talent, clients, and margin from the first side to the second.

You don’t get to opt out of the split. You only get to choose your side — and the choosing mechanism is unglamorous: whether your firm can systematically turn the people it has into the professionals the next decade requires. Infrastructure, not intentions. Curriculum, not culture-speak. A pathway with names and milestones on it, not a promise that things will work out.

I’ve made this kind of bet before, in 2001, when everyone said the model couldn’t change. The firms that moved early banked twenty years of advantage. The window in front of you is bigger than that one was, and it will not stay open until the outcome is obvious — windows never do.

You are not at the mercy of a dying profession. You are at the front of a dividing one. Build the side you want to be standing on.

Want to know which side of the split your firm is currently on?

Book a 10-minute structural alignment review at calendly.com/skillabilitydemo

In ten minutes we’ll run the two audits with you — your automation exposure and your latent advisory revenue — and show you the development infrastructure that moves a firm from the processing side to the advisory side: structured onboarding, pre-employment testing, and the MAPS Tax Advisor Catalyst, all running inside the software your firm already uses.

Put your next hires through our system. If they don’t pass our modules and aren’t autonomously delivering client-ready work within 45 days, we refund 100% of your enrollment fee and pay your monthly subscription out of our own pocket.

To your firm’s capacity,

Vincent Howard, CPA Managing Partner, Howard, Howard and Hodges Skillability for Accounting Firms

Vincent Howard, CPA has practiced public accounting since 1990. He holds a Master’s degree in Taxation, leads a 50-person multi-state firm, and built the Skillability training platform used by accounting firms nationwide through the PASBA network. His firm was named PASBA Firm of the Year.

© 2026 Skillability for Accounting Firms. 45-Day Out-of-Pocket Performance Guarantee applies to qualifying onboarding engagements. Contact us for full terms.